Our Mortgage Programs

Our Mortgage

Programs

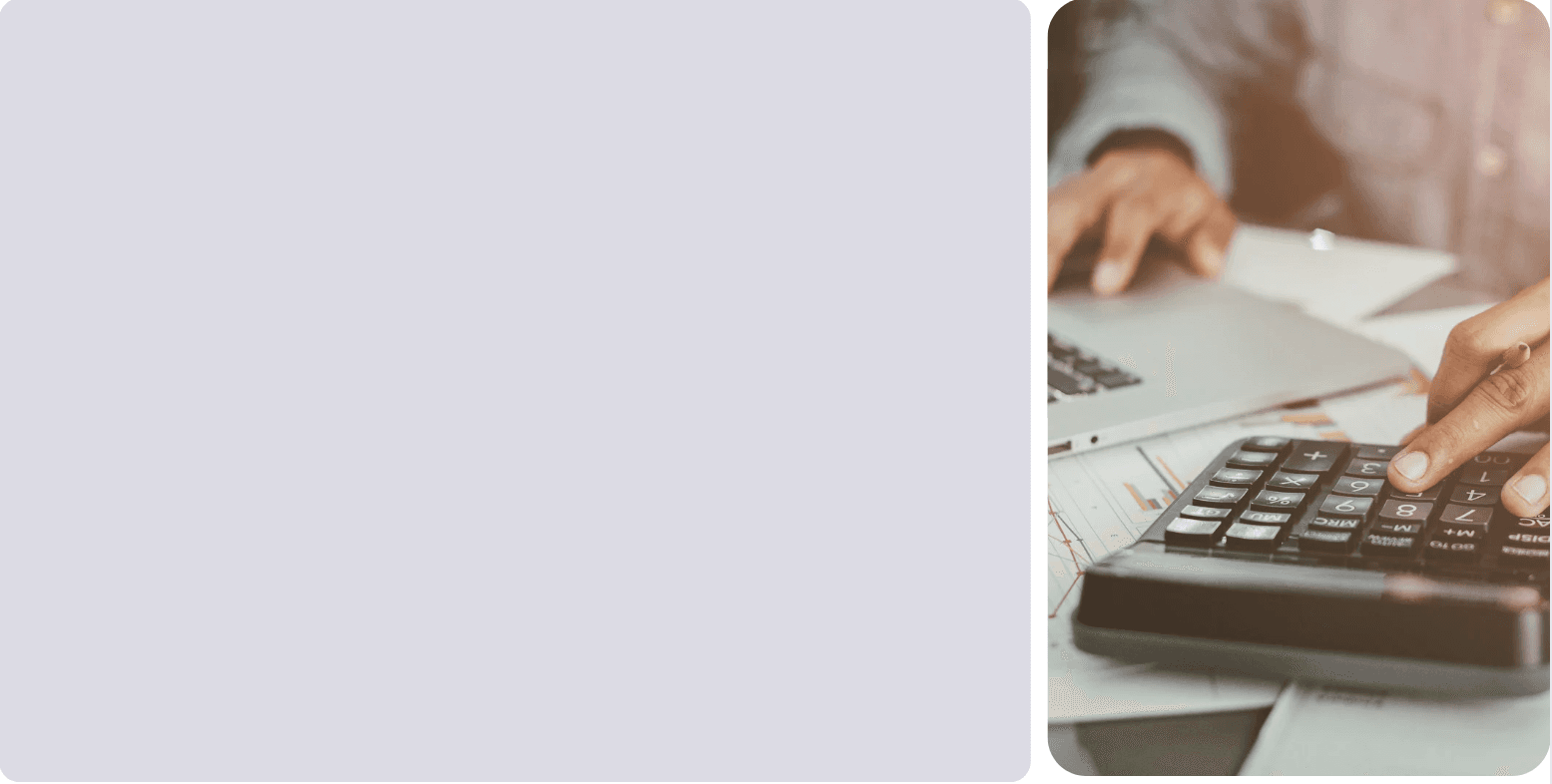

Your dream home is within reach! Let’s find the perfect loan option for you.

Contact us today

Apply Here

BUY YOUR HOME

Your dream home is within reach! Let’s find the perfect loan option for you.

Contact us today

Apply Here

BUY YOUR HOME

PROGRAM

PROGRAM

1. Conventional Loan Products

Who It’s For:

Ideal for applicants with stable income and strong credit scores. Perfect for both purchasing and refinancing your home.

Highlights:

Credit Requirements: FICO scores of 620 and above

Flexible Down Payment: Options starting at 3%

Refinance Options:

Rate & Term Refinance

Cash-Out Refinance

Additional Flexibility: Temporary rate buy-down options and down payment assistance available

We offer a range of mortgage programs designed to meet the unique needs of every homebuyer. Whether you have a stable income and strong credit or are self-employed or managing complex finances, our tailored solutions help you achieve your homeownership goals.

We offer a range of mortgage programs designed to meet the unique needs of every homebuyer. Whether you have a stable income and strong credit or are self-employed or managing complex finances, our tailored solutions help you achieve your homeownership goals.

2. Government Loans (FHA, VA, USDA)

Who It’s For:

Designed to make homeownership more accessible, these programs offer flexible credit criteria. They’re ideal for first-time homebuyers, eligible veterans, active-duty military, and buyers in rural areas. Available for both purchases and refinances.

Program Details:

FHA Loans:

Best for first-time homebuyers with lower credit scores

FICO scores as low as 500 are considered

VA Loans:

Exclusive benefits for eligible veterans and active-duty military

Often include no down payment options

Flexible credit requirements (FICO as low as 500)

USDA Loans:

Supports homebuyers in rural areas with low or moderate incomes

FICO requirements typically start at 620 (for AUS-based files)

Highlights:

Credit Flexibility: Manual underwriting options available

Higher Tolerances: Accommodates lower credit scores and higher debt-to-income ratios

2. Government Loans (FHA, VA, USDA)

Who It’s For:

Designed to make homeownership more accessible, these programs offer flexible credit criteria. They’re ideal for first-time homebuyers, eligible veterans, active-duty military, and buyers in rural areas. Available for both purchases and refinances.

Program Details:

FHA Loans:

Best for first-time homebuyers with lower credit scores

FICO scores as low as 500 are considered

VA Loans:

Exclusive benefits for eligible veterans and active-duty military

Often include no down payment options

Flexible credit requirements (FICO as low as 500)

USDA Loans:

Supports homebuyers in rural areas with low or moderate incomes

FICO requirements typically start at 620 (for AUS-based files)

Highlights:

Credit Flexibility: Manual underwriting options available

Higher Tolerances: Accommodates lower credit scores and higher debt-to-income ratios

2. Government Loans (FHA, VA, USDA)

Who It’s For:

Designed to make homeownership more accessible, these programs offer flexible credit criteria. They’re ideal for first-time homebuyers, eligible veterans, active-duty military, and buyers in rural areas. Available for both purchases and refinances.

Program Details:

FHA Loans:

Best for first-time homebuyers with lower credit scores

FICO scores as low as 500 are considered

VA Loans:

Exclusive benefits for eligible veterans and active-duty military

Often include no down payment options

Flexible credit requirements (FICO as low as 500)

USDA Loans:

Supports homebuyers in rural areas with low or moderate incomes

FICO requirements typically start at 620 (for AUS-based files)

Highlights:

Credit Flexibility: Manual underwriting options available

Higher Tolerances: Accommodates lower credit scores and higher debt-to-income ratios

2. Government Loans (FHA, VA, USDA)

Who It’s For:

Designed to make homeownership more accessible, these programs offer flexible credit criteria. They’re ideal for first-time homebuyers, eligible veterans, active-duty military, and buyers in rural areas. Available for both purchases and refinances.

Program Details:

FHA Loans:

Best for first-time homebuyers with lower credit scores

FICO scores as low as 500 are considered

VA Loans:

Exclusive benefits for eligible veterans and active-duty military

Often include no down payment options

Flexible credit requirements (FICO as low as 500)

USDA Loans:

Supports homebuyers in rural areas with low or moderate incomes

FICO requirements typically start at 620 (for AUS-based files)

Highlights:

Credit Flexibility: Manual underwriting options available

Higher Tolerances: Accommodates lower credit scores and higher debt-to-income ratios

3. Non-Qualified Mortgages (Non-QM)

Who It’s For:

Ideal for applicants who do not meet the strict criteria of traditional loans. These programs offer more flexible underwriting, making them a great choice for self-employed individuals, investors, or those with unique financial circumstances. Note that Non-QM products typically require a higher down payment than conventional or government loans.

Highlights:

Flexible Underwriting:

Accepts bank statements, DSCR loans, profit & loss statements, 1099 income, or alternative income verification

Income Calculation: Based on one year of income

DTI Flexibility: Debt-to-income ratios up to 55% allowed

Product Options: Available for both purchases and refinances

Special Features: Interest-only loan options and no tax returns required

3. Non-Qualified Mortgages (Non-QM)

Who It’s For:

Ideal for applicants who do not meet the strict criteria of traditional loans. These programs offer more flexible underwriting, making them a great choice for self-employed individuals, investors, or those with unique financial circumstances. Note that Non-QM products typically require a higher down payment than conventional or government loans.

Highlights:

Flexible Underwriting:

Accepts bank statements, DSCR loans, profit & loss statements, 1099 income, or alternative income verification

Income Calculation: Based on one year of income

DTI Flexibility: Debt-to-income ratios up to 55% allowed

Product Options: Available for both purchases and refinances

Special Features: Interest-only loan options and no tax returns required

1. Conventional Loan Products

Who It’s For:

Ideal for applicants with stable income and strong credit scores. Perfect for both purchasing and refinancing your home.

Highlights:

Credit Requirements: FICO scores of 620 and above

Flexible Down Payment: Options starting at 3%

Refinance Options:

Rate & Term Refinance

Cash-Out Refinance

Additional Flexibility: Temporary rate buy-down options and down payment assistance available

1. Conventional Loan Products

Who It’s For:

Ideal for applicants with stable income and strong credit scores. Perfect for both purchasing and refinancing your home.

Highlights:

Credit Requirements: FICO scores of 620 and above

Flexible Down Payment: Options starting at 3%

Refinance Options:

Rate & Term Refinance

Cash-Out Refinance

Additional Flexibility: Temporary rate buy-down options and down payment assistance available

Maximize your home's benefits. Lower your rate, lower the Term, Or access your equity.

Contact us today

Maximize your home's benefits. Lower your rate, lower the Term, Or access your equity.

Contact us today

Apply Here

Apply Here

Check Your Rate

Check Your Rate

REFINANCE YOUR HOME

REFINANCE

YOUR HOME

OWNLAND CAPITAL NMLS #2664445 - 40900 Woodward Ave Ste 111 Bloomfield Hills, MI 48304

OWNLAND CAPITAL nmls#2664445

40900 Woodward Ave Ste 111

Bloomfield Hills, MI 48304

OWNLAND CAPITAL

NMLS #2664445

40900 Woodward Ave Ste 111

Bloomfield Hills, MI 48304